Carbon Markets

The MidSEFF Carbon Market Development Support Programme aims to contribute to the creation of an enabling environment for a scaled up domestic carbon market. Carbon pricing and related carbon market activities are an important policy tool that can help Turkey meet its sustainable development objectives, in particular with regards to meeting its Intended Nationally Determined Contribution (INDC) targets in a cost-effective way or even allow Turkey to increase their mitigation ambition . This page offers information on the role Turkey plays in the international carbon market, and the progress Turkey has booked on ETS developments. For more information on CORSIA , the role of carbon markets in the COVID-19 recovery , and the EU’s Carbon Border Adjustment Mechanism , please refer to the drop down menu in the tab at the top of this page.

Turkey and the Paris Agreement

On 12 December 2015, 196 Parties to the UN Framework Convention on Climate Change (UNFCCC) adopted the Paris Agreement, a legally-binding framework for an internationally coordinated effort to tackle climate change. The Agreement represented the culmination of six years of international climate change negotiations under the auspices of the UNFCCC. It requires countries to formulate progressively more ambitious climate targets – Nationally Determined Contributions (NDCs), which are consistent with decarbonisation pathways implied by the Paris Agreement.

For Turkey, this agreement represents a crucial opportunity to transition to a low carbon development pathway while benefitting from international collaboration through international carbon markets. While its special designation under the Kyoto Protocol as an “advanced developing country” meant that Turkey was unable to fully participate in these markets (namely the Clean Development Mechanism) previously, Turkey’s signing of the Paris Agreement in April 2016 marked an important step in linking future domestic mitigation action with international market mechanisms introduced under the Paris Agreement.

It is evident that rapid implementation of mitigation action is urgently needed, and leveraging international carbon markets will be vital to catalyse the volumes of finance required to stimulate this transition. Participation in international carbon markets can offer opportunities for Turkey: in the 2020 – 2030 period as a seller of cost-efficient emission reductions; while post-2030 as a buyer by means of allowing access to lower cost abatement abroad (see study on the economic impacts of collaboration under Article 6). The modalities for accessing new markets established under the Paris Agreement should become clearer during this year’s UN Climate Summit (COP 26), which is to be held in Glasgow in November 2021.

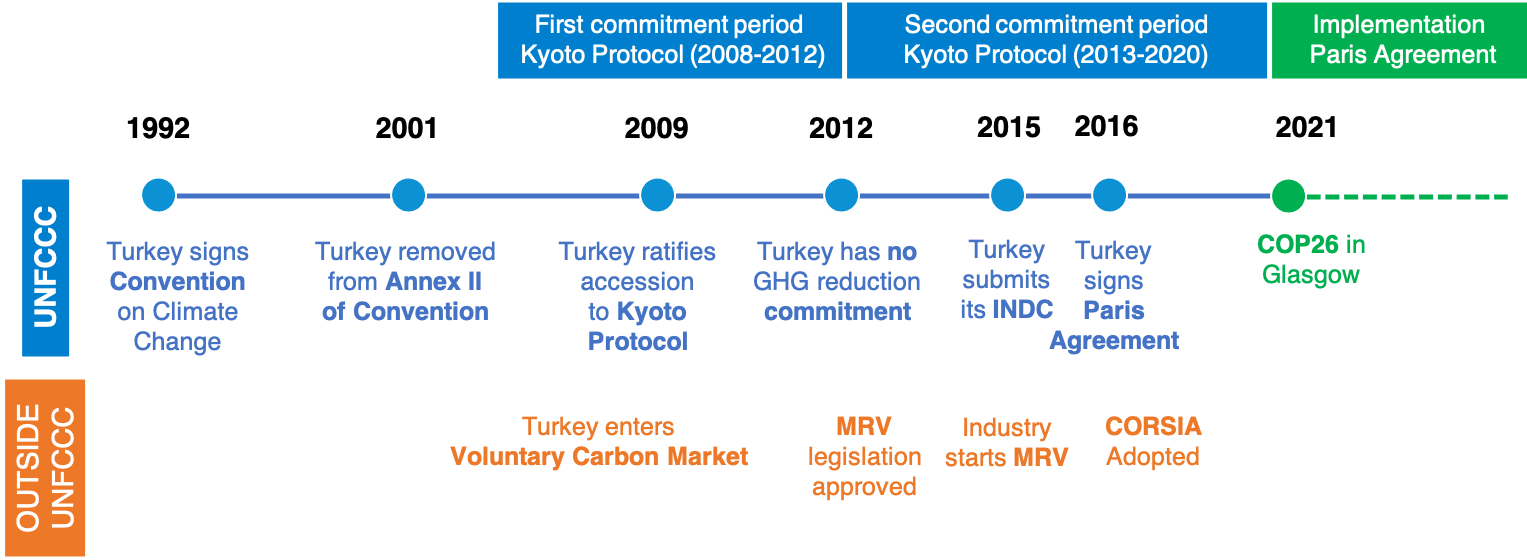

Figure: Timeline of climate policy developments

| -------------- |

|

Source: Climate Focus and GAIA, 2021

Carbon markets in Turkey

The voluntary carbon market relates to transactions in carbon credits that fall outside of compliance schemes. Demand for carbon credits in this market is driven largely by companies and entities that pursue voluntary decarbonisation strategies and intend to demonstrate climate leadership by taking on carbon neutrality or net zero emissions targets, but also for companies in the ‘hard to abate’ sectors, to adequately prepare for carbon transitional risks. The international voluntary market has rebounded in recent years, with transacted volumes doubling since 2017. In 2019, over 100 million tonnes were transacted, with the market value exceeding US$300 million; while official data for the 2020 is not yet available, despite the Covid-19 pandemic, interest for voluntary carbon credits has remained strong.

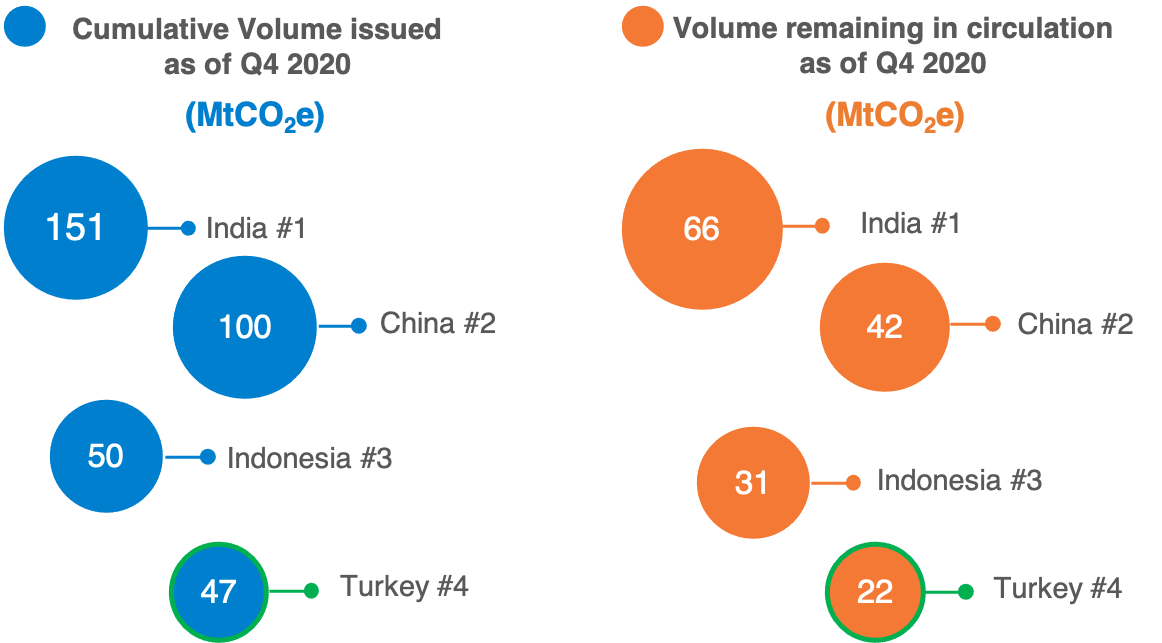

While its categorisation as an Annex I country initially prevented Turkey from benefitting from the market-based mechanisms under the Kyoto Protocol, the country has successfully attracted low-carbon investments by acting as one of the world’s leading host countries under the voluntary carbon market. Turkey is the third-largest host country in terms of number of registered projects (288 as of Q4 2020), and represents the largest seller of voluntary carbon credits in the region.

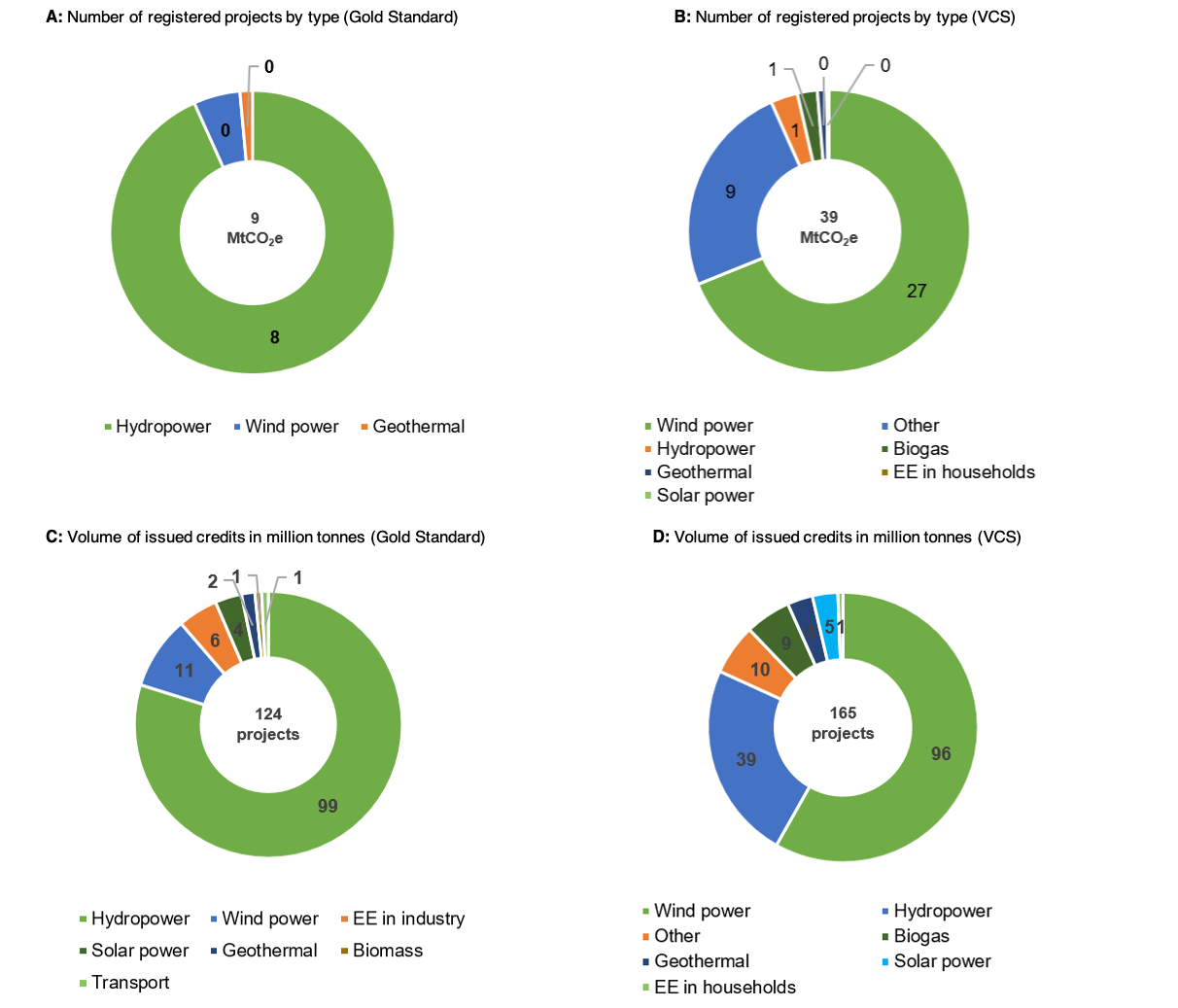

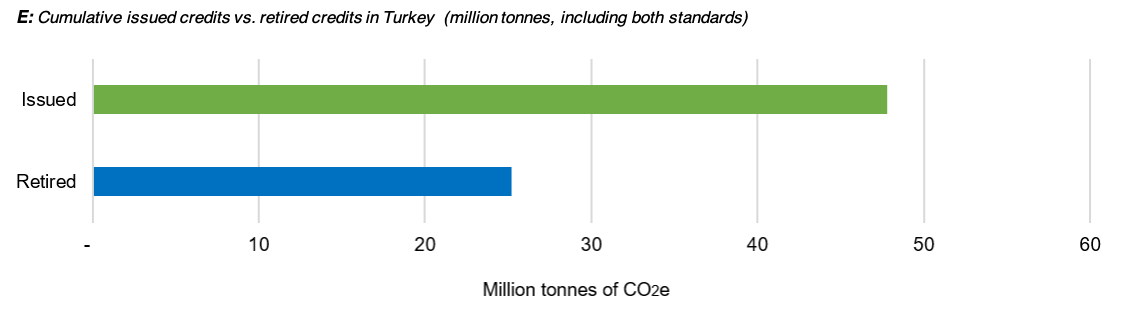

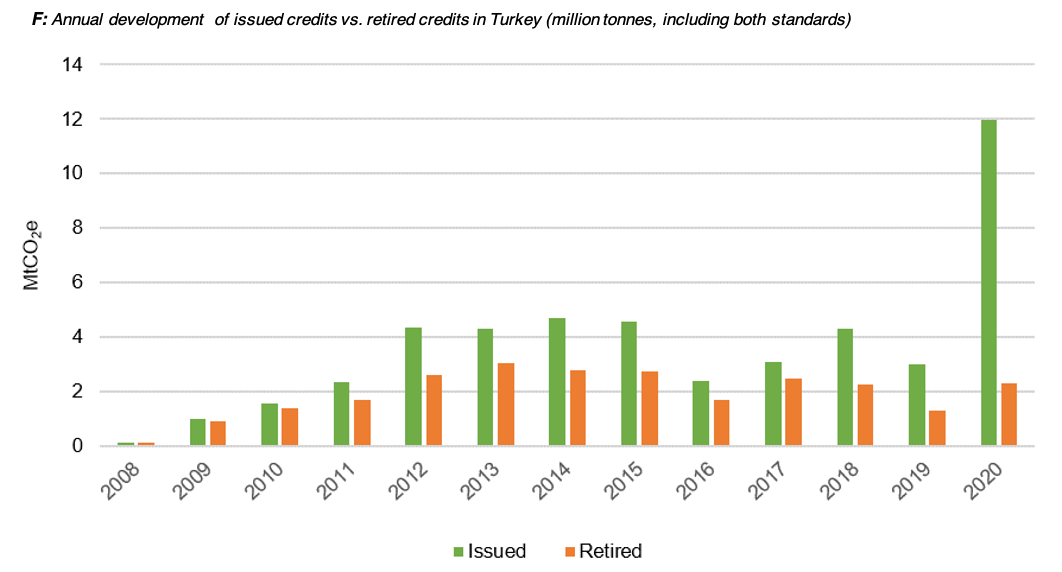

Turkish carbon projects are developed primarily under one of the following two standards: the Gold Standard (SustainCERT) and the Verra’s VCS . Both standards stand out as internationally respected frameworks for the development and implementation of emission reduction projects and are leading global offset standards. As of Q4 2020, Turkey had 165 projects registered under the Gold Standard, and a further 123 under the VCS. The figure below features a dashboard of the Turkish project portfolio for each of the two carbon standards, distinguishing between registered project types, issued volumes, and remaining volumes in the market.

Figure: Role of Turkey in the global voluntary carbon market

| ---------------------------------------- |

|

Figure: Turkey's carbon market dashboard (Q4 2020 data)

| ------------------------------ |

|

| -------------------------- --- |

|

| ---------------------------- |

|

Source: Climate Focus 2021, data taken from the Gold Standard and VCS public registries

Link to emissions trading

In the European Union, a cap-and-trade legislation is in place regulating the amount of greenhouse gases emitted by major installations. The EU emissions trading scheme (EU ETS) has been the region’s key policy tool for containing rising greenhouse gas emissions over the past two decades, and remains a fundamental pillar of the EU Green Deal, which commits the region to reach carbon neutrality by 2050. Through the strong trading ties with the EU, many commercial clients of Turkish banks are directly or indirectly exposed to the prices of emission allowances traded under the EU ETS.

The EU ETS is entering its fourth phase as of 1 January 2021, which will further tighten the overall emissions cap (by 2.2% each year, compared to a reduction of 1.74% per year in the third phase). As a result of EU’s commitment to raise its climate target to a 55% reduction by 2030, tightening allocation rules and the Market Stability Reserve, the price of traded EU allowances has been rising, breaching the EUR30 per tonne mark in Q4 2020.

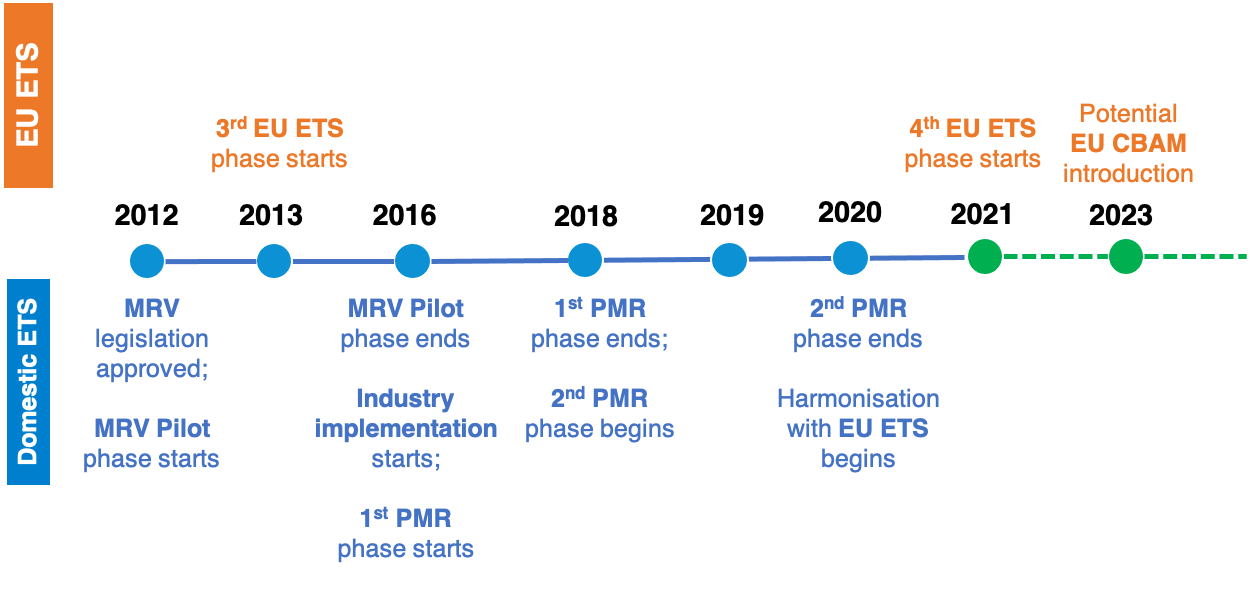

Turkey is taking steps to prepare its economy for closer ties with EU legislation. One important step towards this integration has been the preparation of new legislation to monitor and verify emissions across a range of sectors. The legislation, which was enacted in April 2012, implements key parts of the EU Monitoring Mechanism Decision 280/2004/EC and establishes an installation-level MRV system for close to 1,000 installations. Sectors covered under the regulation include the energy sector (combustion fuels >20MW) and industry sectors (cement, metals, coke production, paper and pulp, glass, ceramic products, insulation materials, and chemicals). All regulated installations in these sectors were obliged to report their 2015 emissions before end of April 2016, and have been reporting their emissions since.

Figure: Timeline of ETS developments

| ---------------------- |

|

Source: Climate Focus and GAIA, 2021

Further support work is currently being undertaken through the World Bank’s Partnership for Market Readiness (PMR), which is supporting Turkey with the development of domestic market-based instruments including the establishment of a national ETS. In November 2018 a synthesis report was submitted to the Climate Change and Air Management Coordination Board, outlining possible carbon market policy options for Turkey. Following this, the end of the year saw the completion of the primary phase, and beginnings of the second phase of the plan. Supported in part with finance from the PMR, the second phase – expected to be complete by the end of 2020 – includes:

- development of a ‘Climate Change Law’, ETS regulation and institutional framework for a pilot ETS

- development of the pilot ETS cap and preliminary specifications for MRV sectors

- development of Turk-SIM (an ETS digital simulation with gamification features)

- development of the pilot ETS transaction registry

- assessment of Article 6 implications and options for Turkey

To find out more about the PMR programme in Turkey, please click here.

Other organisations involved in carbon pricing initiatives in Turkey include the International Carbon Action Partnership (ICAP) and the German Gesellschaft für Internationale Zusammenarbeit (GIZ). To find out more about ICAP's support to Turkey, please click here , and to find out more about GIZ's support to Turkey, please click here .

Turkey’s G

HG emissions outlook

HG emissions outlook

An upper middle-income country with a population of 84 million, Turkey boasts a vibrant economy that has averaged around 4,9% over the past 20 years. The country’s rapid development has also increased greenhouse gas emissions across key economic sectors, and in the period 2005-2016, Turkey’s emissions growth was the largest observed across the OECD, at a rate of 49%.

Turkey’s intended Paris Agreement target (INDC) specifies emissions cuts of up to 21% by 2030, compared to a business-as-usual scenario. Following a business-a s-usual scenario, this target allows emissions growth (excluding LULUCF emissions) of up to 80% above 2018 levels. Such a trajectory is not yet aligned with a science-based approaches for keeping warming below at least 2°C. Moreover, projections indicate the Covid-19 pandemic to have had only a small impact on Turkey’s emission trajectory, with emissions expected to have troughed at only 3-5% below 2019 levels by the end of 2020, and expected return to 2019 levels by 2021. As such, additional mechanisms – and significant financial resources from both national and international sources – are needed to align Turkey’s low carbon transition with global ambitions.

The country is working towards developing new domestic policies that will facilitate its transition into a greener growth trajectory. The majority of emissions growth is forecasted to come from its rapidly expanding power sector, which in 2017 accounted for 56% of the country’s 526.3 MtCO2e emissions. Turkey’s 11th development plan, published in 2019, forecasts a growth in primary energy demand of 18% above 2018 levels by the year 2023. To address this, the plan outlines a target to increase domestic electricity production (including coal) by 46% above 2018 levels by 2023; an increase which does include coal, but which also specifies that 38.8% must be from renewables.

Turkey’s INDC submission to the UNFCCC can be found here .

This website is sponsored by the EBRD Shareholder Special Fund as part of the Turkish Mid-Size Sustainable Energy Finance Facility - Carbon Market Development Support Programme.

Contact

- Climate Focus

-

- +31 20 262 10 30

-

Van Diemenstraat 170

1013 CP Amsterdam

The Netherlands